.jpg)

Imagine being able to predict what customers want before they even ask. While a crystal ball may be out of reach, data powered by AI is bringing us remarkably close. In Financial Services (FS), this isn’t just about increased efficiency; it’s about unlocking foresight that can reshape markets, transform customer relationships, and redefine what trust and value mean in a digital economy.

As part of our ‘Forces Affecting Financial Services’ series, we explore how FS firms can harness AI for predictive personalisation and dynamic customer engagement. In this article, we highlight the opportunities and challenges of using AI to deliver truly customer-centric experiences.

AI and predictive personalisation

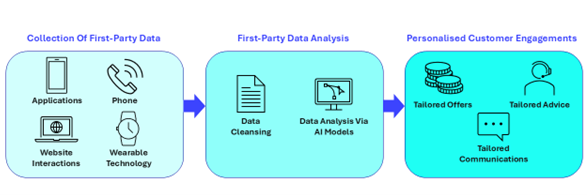

Machine learning techniques can unlock predictive personalisation. This enables businesses to tailor their messaging and products to meet the needs of individual customers. However, this is reliant on clean, first-party data 1 gathered from interactions with customers and their behaviours. AI models can analyse this data, identifying trends that allow firms to forecast customer demand. Based on the predictions, firms can send personalised messages, offers, or advice, delivered through the customer’s preferred channel.

Historically, customers have been grouped by age, income, vulnerability, location, and other factors. This method fails to identify specific, individual preferences. Customers want smooth and timely interactions. Using predictive personalisation helps improve business offerings and meet customer demands. It enables firms to stay competitive and build meaningful relationships with their customers. Using real-time data and AI to predict customer demand effectively addresses this issue. The result is raised customer satisfaction and improved resource allocation. For example, firms can decrease wasteful marketing spending as they have properly determined the target market for each of their product offerings.

Predictive personalisation also enables dynamic customer engagement. This means interacting with customers in real-time, tailoring content, and timing messaging across multiple channels. AI models map customer journeys, directing interactions. This manoeuvres customers to outcomes that meet their demands.

While traditional statistical methods can provide valuable insights, they also have limitations. Dynamic engagements require variables to be analysed across numerous and diverse channels. If data is scattered and sparse, traditional techniques will struggle to make accurate forecasts. In this scenario, AI models and machine learning techniques can identify complex relationships.

Firms that embed AI at the heart of their customer strategy, by harnessing data and building models that deliver truly personalised services, are already seeing step-change results, with some reporting sales conversions that have risen by over 200% (Salesforce). AI is no longer a side experiment; it is fast becoming a defining competitive advantage that will separate tomorrow’s leaders from the rest.

Next-best-action strategies

When suggestions are timely and helpful, customer satisfaction rises. At Morgan Stanley, chatbots offer financial advice based on live interactions (Forbes). AI chatbots could transform the world of work, provided they are trained on clean customer data, grounded in real customer journeys, and backed by strict adherence to regulations.

Next-best-action strategies are only possible when firms have access to clean, connected customer data, spanning transaction history, sentiment, and interactions. With this foundation, AI can analyse profiles in real-time and recommend the most relevant action for each individual. In retail banking, that might mean suggesting a higher-risk portfolio to a young investor with the appetite to match; in insurance, it could mean offering life cover to a new parent at exactly the right moment.

The benefits are twofold: higher customer satisfaction and stronger opportunities for cross- and up-selling. When suggestions are timely and useful, customers feel understood and valued.

The commercial impact is clear. JPMorgan Chase, for instance, has unlocked roughly $2 billion in value by using AI to recommend products tailored to customer behaviour (Forbes). But success at scale requires more than experimentation. To deploy next-best-action strategies externally, firms must ensure mature data management and robustly optimised models, anchored in real customer journeys and designed within strict regulatory boundaries.

Data maturity:

- Refers to how well a firm manages, integrates, and uses its data infrastructure.

- It is necessary to deploy AI models reliant on customer data.

- Data maturity is achieved when data is:

- Clean and free from errors.

- Integrated and unified.

- Real-time and easily accessible.

- Compliant, adhering to regulations.

AI model effectiveness:

- The success of AI deployment is dependent on model optimisation.

- Effective AI models should be:

- Explainable, with transparent reasoning behind all recommendations.

- Tailored to individual customer demands.

- Scalable and capable of handling many interactions across multiple platforms.

- Adaptive to new data sources.

- Bias-mitigated, avoiding discrimination or unethical practices.

Please refer to the following diagram, which emphasises how the successful implementation of next-best-action strategies is achieved through the building blocks of data maturity and optimised AI models.

The need for mature data and optimised models was highlighted in NVIDIA’s ‘State of AI in Financial Services’ 2024 report (NVIDIA). While 75% of institutions claimed to have competitive or leading AI capabilities, data issues were the biggest barrier to achieving their goals. In contrast, firms with mature data and optimised AI models saw clear benefits:

- A 30% increase in the speed of AI deployment.

- A 25% rise in customer satisfaction.

- A 20% boost in cross-sell and up-sell conversion rates.

This suggests that the success of an AI model depends on its inputs and configuration.

Considering the risks

Using AI models carries significant risks. The biggest concerns are a lack of explainability, poor transparency, weak governance, issues such as bias and overfitting, and regulatory non-compliance.

The following aspects of AI must be considered to limit exposure to risk wherever possible:

- AI can produce results that are difficult to interpret: If decisions cannot be explained, firms will fall short of the requirements set by the FCA, PRA, or the EU AI Act.

- Breach of these rules can result in fines of up to €35 million or 7% of global annual turnover (EU AI Act).

- fear of breaching regulations and incurring financial penalties

- Firms can experiment with AI using the new FCA ‘Supercharged Sandbox’. This allows firms to test AI models without the fear of breaching any regulations and being financially penalised (FCA).

- Regulatory compliance is crucial: AI implementations must adhere to strict rules to avoid the risk of fines and reputational damage:

- UK regulators, such as the FCA and PRA, stress due diligence, transparency, bias mitigation, and governance.

- UK GDPR laws emphasise data security and customer protection.

- The EBA details that AI should ensure ethical outcomes and, above all else, customers must be protected.

- Lack of transparency breaks trust: If customers or investors do not understand how decisions are made, confidence in the system starts to decline. Once trust is lost, it’s very difficult to restore.

- New data can introduce unpredictability: If organisations do not know how a model works, they cannot predict how it’ll react to new inputs. This puts both reputation and profits at risk.

- Proper governance is essential: The Global Risk Institute has warned that without governance, AI could increase systemic risk, especially in areas like credit scoring or trading (The Global Risk Institute). Good governance involves:

- Validating models.

- Monitoring performance.

- Maintaining human oversight.

- Documenting how models are trained and configured.

- Bias is a major issue: This happens when training data reflects social inequalities. Indeed, some banking models have offered lower credit limits for women than for men with the same profile (CNBC).

- Overfitting is a concern: This is when a model performs well on training data but has performance issues in the real world.

- Risk management: The key steps are:

- Regular bias testing.

- Training models on diverse, representative data.

- Keeping human oversight in all AI processes.

AI is rapidly becoming a core driver of value creation

Firms that fail to seize this opportunity risk being left behind. Despite the risks and regulations, data, when powered by AI, offers significant and valuable benefits. Personalisation is becoming a key advantage for early adopters. It helps create tailored customer journeys that promote customer loyalty and bolster profits. Indeed, generative AI and personalisation could deliver up to $340 billion in value each year for the banking industry alone (McKinsey).

As this article has highlighted, the practical implementation of AI is a complex process. It requires a clear strategy, deep expertise, and careful consideration of regulations. At Lancia Consult, we understand both the business and technical aspects of AI implementations. We are equipped to help firms manage their transformation. We can support you in:

- Aligning AI with your business goals.

- Building the right level of data maturity.

- Integrating AI with legacy systems.

- Navigating regulatory compliance.

- Designing intelligent customer journeys.

- Embedding next-best-action strategies.

Discover how these concepts drive real-world impact by reading our case study on how we helped a top FS firm boost customer engagement by overhauling its client data management system.

To stay competitive, transformation is essential. Are you ready to take the leap with us? Contact a member of our team today to start the conversation.

References

1 First-party data is that which is collected directly by an organisation through its interactions with customers, as opposed to third-party data, which is collected from external sources that do not directly interact with the customer. First-party data is collected from various sources, including applications, phone calls and messages, website interactions, and wearable technology.

-

.png)